Medical Aid

Medical aid covers members' healthcare costs such as hospitalisation, treatments and medicine. These costs are covered according to the rules of the medical scheme and the member's medical aid plan type. These rules ensure that members are fairly cared for.

There are two kinds of medical schemes, namely, open and closed (restricted) schemes. Any person can join an open scheme, but closed schemes are for the employees of specific employer groups or membership of a particular profession, industry, association or union.

A hospital plan covers treatment and medical costs that arise while the insured is booked into hospital, while a comprehensive medical aid plan will cover hospital costs and other private medical needs like specialist consultations, GP visits, and additional tests or procedures

According to the Medical Schemes Act, medical aid schemes are entitled to impose a 3 months general waiting period and / or a 12 months condition specific waiting period(s) for any pre-existing medical condition(s).

Medical aid in South Africa provides financial cover for medical expenses for members who pay a monthly contribution for this cover. These contributions are paid to medical aid schemes (including Discovery Health Medical Scheme) and are pooled and safeguarded. These schemes are operated on a not-for-profit basis.

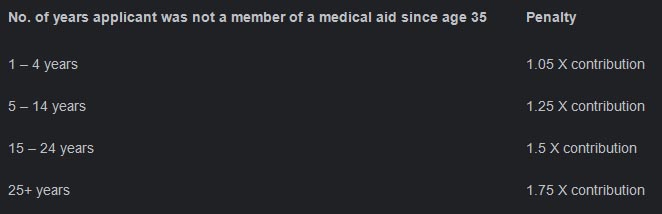

Late Joiner Penalty

A late-joiner penalty is a higher monthly rate you pay for membership because you only join a medical scheme at a later stage in life when you are more likely to need expensive cover from a medical scheme.

How is late joiner penalty calculated?

We determine the applicable penalty band as shown in the table above and based on the following formula as described in the Medical Schemes Act: X - (35 + Y) = Z, where: X is the age of the late joiner at the time of their application for membership or admission as a dependant.

How long does late joiner penalty last?

This penalty (known as a late-joiner penalty) is added onto the monthly contribution and remains with the member for life. It is important to note that any cover the member may have had under the age of 21 is excluded. The penalty is applied based on the risk contribution payable to the medical scheme.

What are Prescribed Minimum Benefits?

Prescribed Minimum Benefits (PMBs) are a set of defined benefits to ensure that all medical scheme members have access to certain minimum health services, regardless of the benefit option they have selected. The aim is to provide people with continuous care to improve their health and well-being and to make healthcare more affordable.

PMBs are a feature of the Medical Schemes Act, in terms of which medical schemes have to cover the costs related to the diagnosis, treatment and care of:

- any emergency medical condition

- a limited set of 271 medical conditions (defined in the Diagnosis Treatment Pairs)

- 26 chronic conditions (defined in the Chronic Disease List)

When deciding whether a condition is a PMB, the doctor should only look at the symptoms and not at any other factors, such as how the injury or condition was contracted. This approach is called diagnosis-based. Once the diagnosis has been made, the appropriate treatment and care is decided upon as well as where the patient should receive the treatment (at a hospital, as an outpatient or at a doctor’s rooms).

PMB Definitions

The legislation governing the provision of the prescribed minimum benefits (PMBs) is contained in the regulations enacted under the Medical Schemes Act, 1998 (Act No. 131 of 1998).

In respect of some of the diagnosis treatment pairs (DTPs), medical scheme beneficiaries find it difficult to know their entitlements in advance, while medical schemes interpret these benefits differently, resulting in a lack of uniformity of benefit entitlements.

The benefit definition project is coordinated by the CMS, with the aim to define the PMB package; and to guide the interpretation of the PMB provisions by relevant stakeholders.

The guidelines are based on evidence of clinical and cost effectiveness, taking into consideration affordability constraints and financial viability of medical schemes in South Africa.

Why do we have PMBs?

There are two main reasons why PMBs were created:

To ensure that medical scheme beneficiaries have continuous healthcare. This means that even if a member’s benefits for a year have run out, the medical scheme has to pay for the treatment of PMB conditions; and

To ensure that healthcare is paid for by the correct parties. Medical scheme members with PMB conditions are entitled to the specified treatments and these have to be covered by their medical scheme, even if the patients were treated at a state hospital.

But there are other valid reasons too:

To provide minimum healthcare to everybody who needs it, regardless of their age, state of health or the medical scheme cover option they belong to;

PMBs have a part to play in ensuring that medical schemes remain financially healthy. When beneficiaries receive good care on an ongoing basis, their general wellness improves, resulting in fewer serious conditions that are expensive to treat;

and to ensure that healthcare is paid for by the correct parties. Medical scheme members with PMB conditions are entitled to the specified treatments and these have to be covered by their medical scheme, even if the patients were treated at a state hospital.

Which conditions are covered?

The Regulations to the Medical Schemes Act in Annexure A provide a long list of conditions identified as Prescribed Minimum Benefits. The list is in the form of Diagnosis and Treatment Pairs (DTPs).

A DTP links a specific diagnosis to a treatment and therefore broadly indicates how each of the approximately 271 PMB conditions should be treated. The treatment and care of PMB conditions should be based on healthcare that has proven to work best, taking affordability into consideration. Should there be a disagreement about the treatment of a specific case, the standards (also called practice and protocols) in force in the public sector will be applied.

The treatment and care of some of the conditions included in the DTP may include chronic medicine, e.g. HIV-infection and menopausal management. In these cases, the public sector protocols will also apply to the chronic medication.

Here is an example of a DTP as it appears in the Medical Schemes Act:

Code | Diagnosis | Treatment |

| 109A | Vertebral dislocations/fractures, open or closed with injury to spinal cord | Repair/reconstruction; medical management; inpatient rehabilitation up to two months |

The 271 conditions that qualify for PMB cover are diagnosis-specific and include a range of ailments that can be divided into 15 broad categories:

PMB Category | Example |

| Brain and nervous system | Stroke |

| Eye | Glaucoma |

| Ear, nose, mouth and throat | Cancer of oral cavity, pharynx, nose, ear, and larynx |

| Respiratory system | Pneumonia |

| Heart and vasculature (blood vessels) | Heart attacks |

| Gastro-intestinal system | Appendicitis |

| Gastro-intestinal system | Appendicitis |

| Liver, pancreas and spleen | Gallstones with cholecystitis |

| Musculoskeletal system (muscles and bones); Trauma NOS | Fracture of the hip |

| Skin and breast | Treatable breast cancer |

| Endocrine, metabolic and nutritional | Disorders of the parathyroid gland |

| Urinary and male genital system | End-stage kidney disease |

| Female reproductive system | Cancer of the cervix, ovaries and uterus |

| Pregnancy and childbirth | Antenatal and obstetric care requiring hospitalisation, including delivery |

| Haematological, infectious and miscellaneous systemic conditions | HIV/Aids and TB |

| Mental illness | Schizophrenia |

| Chronic conditions | Asthma, diabetes, epilepsy, hypothyroidism, schizophrenia, glaucoma, hypertension |

No exclusions

Medical schemes often have a list of conditions – such as cosmetic surgery – for which they will not pay, or circumstances – such as travel costs and examinations for insurance purposes – under which a member has no cover. These are called exclusions. Exclusions, however, do not apply to PMBs.

If you contract septicaemia after cosmetic surgery, for example, your scheme has to provide healthcare cover for the septicaemia part because septicaemia is a PMB. (Cosmetic surgery remains an exclusion.) PMBs are concerned about the diagnosis; it doesn’t matter how you got the condition.

Which chronic diseases are covered?

The Chronic Disease List (CDL) specifies medication and treatment for the 25 chronic conditions that are covered in this section of the PMBs:

| Chronic renal disease | Addison’s disease | Asthma |

| Bronchiectasis | Cardiac failure | Cardiomyopathy |

| Chronic obstructive pulmonary disorder | Coronary artery disease | Crohn’s disease |

| Diabetes insipidus | Diabetes mellitus types 1 & 2 | Dysrhythmias |

| Epilepsy | Bipolar Mood Disorder | Hypothyroidism |

| Hypertension | Glaucoma | Haemophilia |

| Ulcerative colitis | Systemic lupus erythematosus | Schizophrenia |

| Rheumatoid arthritis | Parkinson’s disease | Hyperlipidaemia |

| Multiple sclerosis |

To manage risk and ensure appropriate standards of healthcare, so-called treatment algorithms were developed for the CDL conditions. The algorithms, which have been published in the Government Gazette, can be regarded as benchmarks, or minimum standards, for treatment. This means that the treatment your medical scheme must provide for may not be inferior to the algorithms.

If you have one of the 25 listed chronic diseases, your medical scheme not only has to cover medication, but also doctors’ consultations and tests related to your condition. The scheme may make use of protocols, formularies (lists of specified medicines) and Designated Service Providers (DSPs) to manage this benefit.

What happens in an emergency?

An emergency medical condition means the sudden and, at the time, unexpected onset of a health condition that requires immediate medical treatment and/or an operation. If the treatment is not available, the emergency could result in weakened bodily functions, serious and lasting damage to organs, limbs or other body parts, or even death.

In an emergency it is not always possible to diagnose the condition before admitting the patient for treatment. However, if doctors suspect that the patient suffers from a condition that is covered by PMBs, the medical scheme has to approve treatment. Schemes may request that the diagnosis be confirmed with supporting evidence within a reasonable period of time.

What are ICD-10 codes?

One of the types of codes that appear on healthcare provider accounts is known as ICD-10 codes. These codes are used to inform medical schemes about what conditions their members were treated for so that claims can be settled correctly.

ICD-10 stands for International Classification of Diseases and Related Health Problems (10th revision). It is a coding system developed by the World Health Organisation (WHO), that translates the written description of medical and health information into standard codes, e.g. J03.9 is an ICD-10 code for acute tonsillitis (unspecified) and G40.9 denotes epilepsy (unspecified).

When you join a medical scheme, you choose and pay for a particular benefit option. This benefit option contains a basket of services that often has limits on the health services that will be paid for. Because ICD-10 codes provide accurate information on the condition you have been diagnosed with, these codes help the medical scheme to determine what benefits you are entitled to and how these benefits could be paid.

This becomes very important if you have a PMB condition, as these can only be identified by the correct ICD-10 codes. Therefore, if the incorrect ICD-10 codes are provided, your PMB-related services might be paid from the wrong benefit (such as from your medical savings account), or it might not be paid at all if your day-to-day or hospital benefits limits have been exhausted.

ICD-10 codes must also be provided on medicine prescriptions and referral notes to other healthcare providers (e.g. pathologists and radiologists) who are not all able to make a diagnosis. Therefore, they require the diagnosis information from your referring doctor so that their claim to your medical scheme can also be paid out of the correct pool of money.

Important note: Medical schemes are obliged by law to treat information about members’ conditions with the utmost confidentiality. They are not allowed to disclose even ICD-10 codes to any other party, including employers or family members.

Gap cover

Gap Cover is a short term insurance product for members of a medical scheme, providing extra cover for medical shortfalls that could occur during in-hospital procedures.

Medical aid VERSUS Medical Insurance

Medical aid ensures you are covered if you need to be hospitalised, have a chronic condition under prescribed minimum benefits or need day-to-day benefits. However, medical insurance ensures you receive a pay-out if you are hospitalised and cannot work or earn a living.